Are You a Sole Proprietor? Which Retirement Plan is Best for You?

If you are a successful independent contractor, sole-proprietor, or gig worker, you have several options to save for retirement and reduce taxable income. SEP IRA and Solo 401(k) plans are designed to maximize retirement savings for the self-employed. However, each type of plan has distinct differences that should be evaluated to determine which plan is right for you.

Joan was a Director of Supply Chain Management at a large Health Care company. Unfortunately, the COVID crisis forced the Company to offer early retirement incentives to offset the sudden decrease in demand for its products. Joan had dreamt of starting her own consulting practice, so she jumped at the chance to leave her corporate job with a nice cushion. Joan’s skills were in great demand and she soon began to earn more fees than her previous salary. Joan wanted to continue to save for retirement in a tax efficient way but wasn’t familiar with retirement plans for the self-employed. What options did she have?

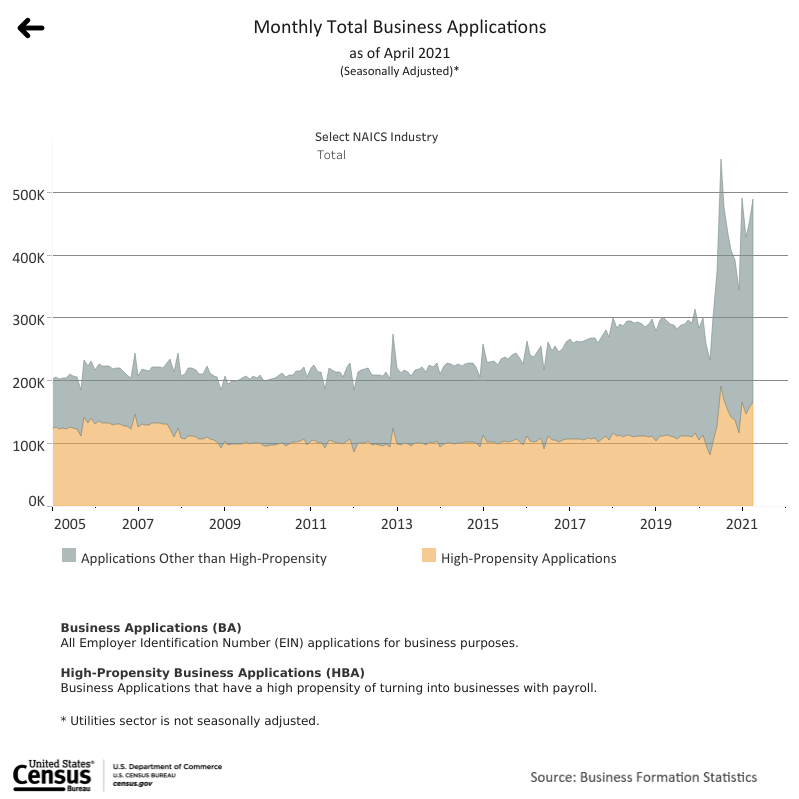

Joan wasn’t alone in her self-employment quest. The United States Census Bureau reported that 2020 had the biggest number of business formations in U.S. history.[1]

Like Joan, the pandemic allowed many employed adults to pursue their dreams and start their own companies. Many of these corporate ex-pats were familiar with the value of saving in a retirement account like a 401(k) and they were determined to establish a plan on a much smaller scale but with similar advantages. Fortunately, two types of plans, the SEP IRA and the Solo 401(k) were designed with these individuals in mind.

What is a SEP IRA?

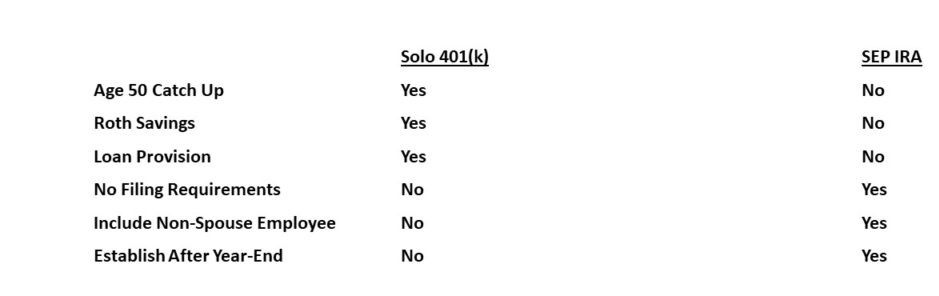

A Simplified Employee Pension or SEP allows employers to contribute to traditional IRA’s on behalf of their employees. A SEP can be established for any size company including the self-employed. It can be created up to the date that they employer files their tax return. Accounts are set up in individuals names (similar to a traditional IRA) and always 100% vested. The employer can contribute up to 25% of each employee’s pay but is based only on the first $290,000 of compensation in 2021. Each employee must receive the same percentage of compensation and is limited annually to the smaller of $58000 or 25% of compensation. For the self-employed, the contribution is based on net earnings from employment reduced by ½ the self-employment tax and SEP contributions. (All calculations should be reviewed by your tax advisor).

Withdrawal rules for A SEP are also like traditional IRA’s. All distributions are taxed at the employee’s federal tax rate at the time of withdrawal and if it occurs prior to age 59 ½, a 10% penalty will be assessed. State tax rules may vary.

There aren’t any annual reporting requirements for SEP IRA’s and the plan can be terminated at any time with proper notifications.

What is a Solo 401(k)?

A Solo 401k, sometimes known as a Uni-k, Solo-k, or One Participant k, is a retirement account designed specifically for Sole Proprietors and their spouses. If the business owner has any employees beyond his or her spouse, they are not eligible for the Solo 401k.

The plan is structured similarly to a traditional, large company 401k with identical contribution limits. However, plan documents are simplified, fees may be much less, and the plan is not subject to many ERISA rules. The plan must be established prior to December 31st.

The Solo 401k has several features that may appeal to an entrepreneur.

- Like a traditional 401k, you can defer $19,500 of your earnings in a pre-tax account. If you are over age 50, you can add $6,500 as a “catch-up” contribution for a total of $26,000.

- A Roth provision can be added to the plan. You can contribute the same amount to this after-tax account as you can to the pre-tax account.

- You can contribute to both pre-tax and after-tax accounts. But you can’t exceed the total salary deferral amount of $19,500 or $26,000 if you are over 50.

- Your company can also add a profit-sharing contribution. This is calculated in the same manner as the SEP IRA.

- The total of salary deferrals and profit sharing cannot exceed $58,000 or $64,500 if you are older than 50.

- Finally, you can add a loan provision to the plan. Although not necessarily recommended, you can borrow from your account balance if the need arises.

Unlike the SEP IRA, a Solo 401(k) may have federal reporting requirements. If the account balance is great than $250,000, the IRS requires that a form 5500 is filed. Also, this form must be submitted if the plan, is terminated

SEP IRA versus Solo 401k

SEP IRA versus Solo 401k – Which is right for me?

The choice between A SEP IRA and a Solo 401k should be made with the help of your tax advisor but here are a few key features that may determine your choice.

The Self Employed have several options to contribute and grow their retirement savings. Both the Solo 401(k) and Sep IRA allow for significant account additions. To properly choose the appropriate option for you, you need a trusted team to help determine the appropriate option. I would be happy to be on your team. Please call me and Let’s Make a Plan!

06/21

Advisory offered through Capital Analysts or Lincoln Investment, Registered Investment Advisors. Securities offered through Lincoln Investment, Broker/Dealer, Member FINRA/SIPC. www.lincolninvestment.com

West Coast Financial Group Inc. the above firms are not affiliated.

Tax services are not offered through, or supervised by Lincoln Investment, or Capital Analysts. None of the information in this document should be considered as tax advice. You should consult your tax advisor for information concerning your individual situation.

The above hypothetical examples are for illustrative purposes only and do not attempt to predict actual results of any particular investment.

There is no guarantee that any strategies discussed will result in a positive outcome. All investing involves risk and no investment strategy can guarantee a profit or protect against loss, including the potential loss of principal.

Diversification does not guarantee a profit or protect against a loss.

[1] United States Census Bureau – Business Formation Statistics April 2021