3 Costly Mistakes You Need to Avoid When Exercising Your Stock Options

Stock options can be a very lucrative form of employee compensation. When I was recruited by a Fortune 50 company for an executive position, options were the most appealing aspect of the compensation package that was offered. Recent initial public offerings (IPO) in shares of companies like AirBnB, Poshmark, and DoorDash have created significant wealth, at least on paper, for those employees fortunate enough to have been awarded stock option grants prior to the offering. If you are one of those employees or an executive at a more established firm that grants stock options as part of your annual compensation, congratulations! But you should be aware that there are several pitfalls that you may encounter when exercising these grants that could significantly reduce the wealth created by the options.

Stock Option Overview

Stock options usually come in two “flavors” – Non-Qualified Stock Options (NQSO) and Incentive Stock Options (ISO). The granting of Non-Qualified Stock Options is more popular than ISO grants.

The two option types have several similarities.

- The company offers a “grant” which outlines a specific number of shares that can be purchased, at a specific time, and at a specific price.

- The option is usually exercised after a certain period has elapsed. This is known as the “vesting period” and it may last for several years.

- They options can expire after several years. After this period, any remaining options can no longer be exercised and are worthless.

NQSO’s and ISO’s also have some differences such as tax treatment, value of the grant, and eligibility requirements.

A much wider slice of people is eligible for NQSO’s than ISO’s so we will focus on Non-Qualified Stock Options.

NQSO’s – The Details

When a company issues a stock option grant, the grant specifies the number of shares that the employee is eligible to purchase. The grant also details when the employee is eligible to purchase these shares. This is referred to as the vesting schedule. The most common types of vesting schedules are cliff vesting and graded vesting.

Vesting

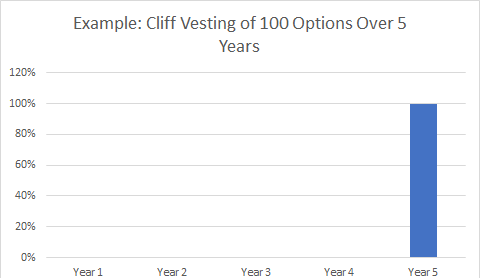

If options are issued using a cliff vesting schedule, many shares are eligible for purchase at one time such as after three or five years.

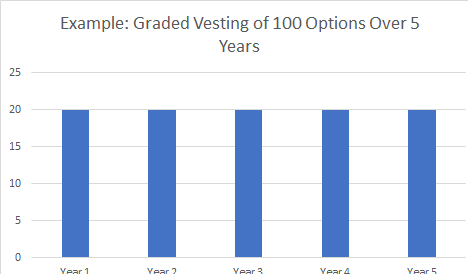

A graded vesting schedule portions the options out over several years.

Exercising the Options

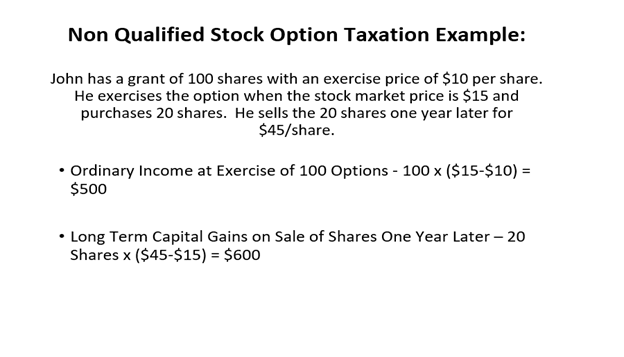

The stock option grant specifies the price at which the share of stock can be purchased. The difference between the grant price and the actual share price at exercise is called the “spread” and is subject to taxation. If the actual price of the shares is lower than the grant price, than the spread is negative. The option is “out of the money” and won’t be exercised. If the price of the shares is higher than the grant price, the spread is positive. The option is “in the money” and may be exercised.

If the option is exercised, the shares are purchased and owned by the grantee. They can be immediately sold or held for future sale or gifting.

Tax Consequences

Nonqualified stock options do not qualify for special federal tax treatment. Proceeds are considered compensation and are subject to all payroll related taxes at the time of exercise. This includes federal, state, and Medicare/Social Security taxes.

At exercise, many option holders will sell sufficient shares to pay the estimated taxes. This is referred to as a cashless exercise.

But What Could Go Wrong? – Three Costly Mistakes

If you are fortunate enough to have received stock options that end up “in the money”, you have an asset which requires proper planning to maximize the value of the grant. Too often, grantees fail to recognize that options which have become a major portion of their net worth don’t manage themselves. Without a defined exit plan, stock option wealth can diminish quickly.

Here are three mistakes that can significantly reduce your wealth.

- Failure to Take Advantage of Long-Term Capital Gains Tax Rates –

Carl received a non-qualified stock option grant of 1000 shares when he was hired by a large technology firm. Sensing that the company was about to enter a growth spurt, Carl waited to exercise his options. Carl was correct. The company grew beyond his expectations and the stock price skyrocketed. In his fifth year of employment, he chose to exercise all of his vested options and receive the proceeds in cash. The following April, his accountant told him that his tax bill was greater than the last five years combined.

Exercising Non-qualified options triggers ordinary income tax rates on the spread between the option grant price and the stock price at the time of exercise. Carl chose to exercise all of his options after a big runup in the stock price, so his entire proceeds were subject to ordinary income taxes. If had exercised some of his options each year and purchased the underlying stock, he could have held those shares longer than the one year required to receive favorable Long Term Capital gains tax treatment. He could then choose to sell the shares at a much lower tax rate.

- Disregarding Diversification

Jennie, a Director of Operations at a small pharmaceutical company, received annual stock option grants as part of her executive compensation package. Each year she chose to exercise some of the options and purchase the underlying company stock. As she approached her retirement, 80% of her net worth was tied to the company’s stock and options. Unfortunately, the company had a string of R&D failures during the year she planned to retire. The stock price was decimated, and her retirement fund was ruined. Jennie postponed her ‘round-the-world cruise.

Although it doesn’t guarantee investment success by itself, diversification could have helped save Jennie’s retirement fund. Diversification may reduce volatility and risk in an investment portfolio. Jennie should have considered purchasing investments other than her company stock when she exercised her options.

- Neglecting to Hedge Large Positions Against Loss

Bob had accumulated significant wealth as CEO of a food services company. For tax reasons, he wished to exercise his options and liquidate his stock once he retired. Unfortunately, the COVID crisis overwhelmed the food service industry and his firm’s performance suffered significantly. Bob’s options expired worthless, and his stock was worth a fraction of its former level. Bob no longer had a tax problem.

Like diversification, there are several hedging strategies that can be used to offset the risk of large, concentrated stock positions. There may be a cost to these strategies but that may be far smaller than the loss that can be experienced by an unforeseen turn in the stock price.

The accumulation of wealth is often determined by making a series of good decisions. In the case of wealth gained by the appreciation of company stock and exercising options, there several tax and financial planning decisions that can be made to increase the probability of success. With the help of a team of trusted advisors, you can increase that probability. I would be happy to be on that team. Please call me and Let’s Make a Plan!

05/2021

Advisory offered through Capital Analysts or Lincoln Investment, Registered Investment Advisors. Securities offered through Lincoln Investment, Broker/Dealer, Member FINRA/SIPC. www.lincolninvestment.com

West Coast Financial Group Inc. the above firms are not affiliated.

Tax services are not offered through, or supervised by Lincoln Investment, or Capital Analysts. None of the information in this document should be considered as tax advice. You should consult your tax advisor for information concerning your individual situation.

The above hypothetical examples are for illustrative purposes only and do not attempt to predict actual results of any particular investment.

There is no guarantee that any strategies discussed will result in a positive outcome. All investing involves risk and no investment strategy can guarantee a profit or protect against loss, including the potential loss of principal.

Diversification does not guarantee a profit or protect against a loss.